Identity verification for banks and financial institutions

Reduce fraud and identity theft, streamline account opening, and improve customer service with our ID scanners for banks and credit unions.

ID verification

Omnichannel identity verification for banks and credit unions

Verify ID and identity remotely

With digital identity verification, you can easily onboard customers, verify identity, and meet KYC/AML standards in seconds. Our three step process includes document validation, and a face matching liveness check.

Scan IDs using the Digital Check SmartSource scanner

The Digital Check scanners are now fully compatible with our ID scanning solutions, allowing for banks to scan IDs into their existing teller lane software with scanners they already have on the floor.

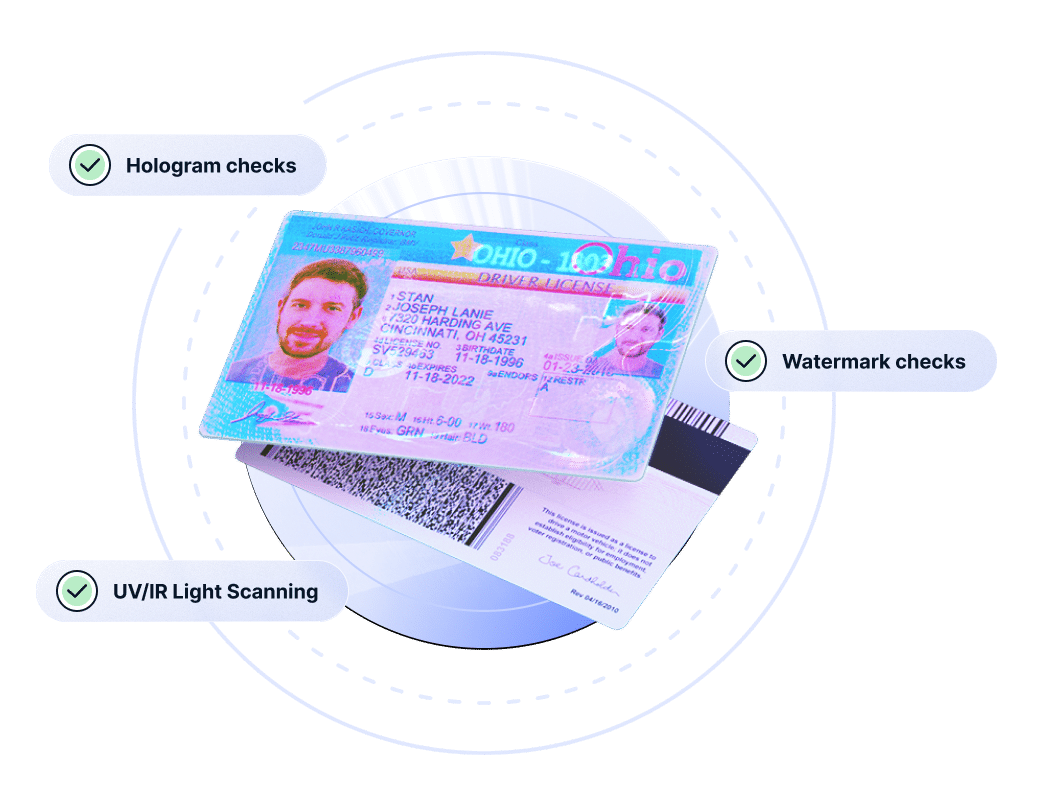

Catch 95% of fake IDs with ID authentication

Specialty hardware can perform forensic document examination under multiple light wavelengths to give deep confidence in the document’s legitimacy.

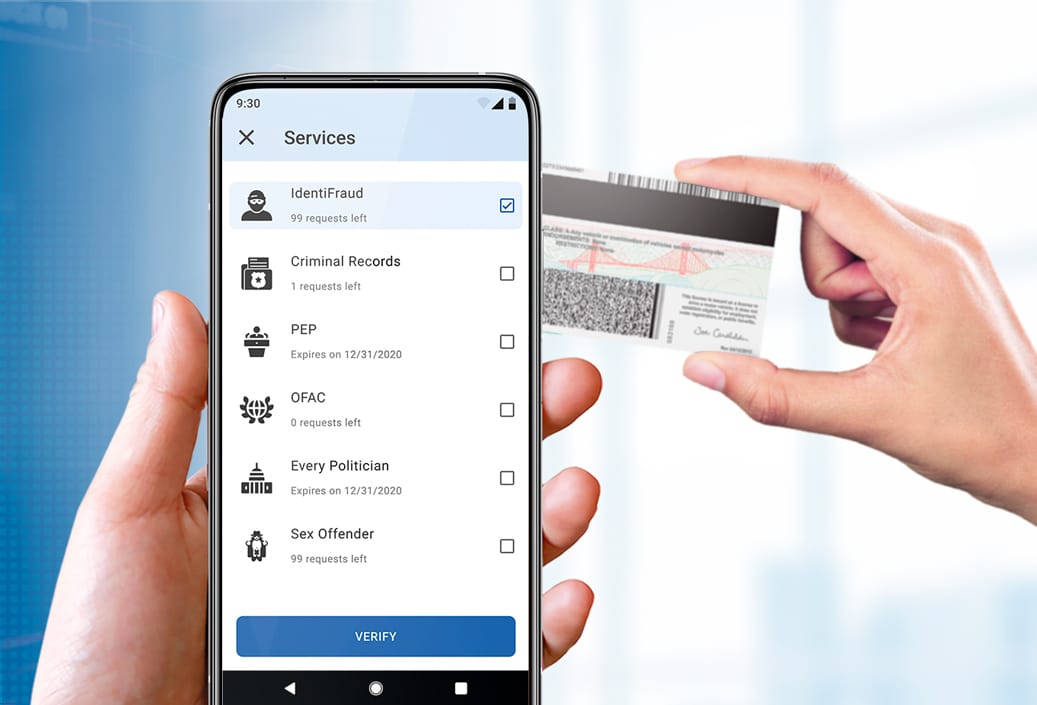

Query external data sources for deeper fraud protection

We offer easy access to state DMV records, Office of Foreign Asset Control lists, Politically Exposed Persons lists, and a propritary multi-risk check called IdentiFraud which checks identity against more than 15 sources.

Banks & Credit Unions

Baking & fintech software integrations

Add ID scanning software to your bank or credit union tech stack. Prevent ID fraud by verifying every identity document. Clean, accurate data is parsed from the ID directly into your key systems directly from the ID scanner.

- Instantly ingest data

- Save an image of each ID

- Sync data directly into your bank’s key software and systems

- Perform security checks on each ID

- Install in minutes

- Streamline account withdrawals, loans, and other processes

Scan IDs into MeridianLink

Prevent ID fraud by verifying every ID, and then send clean data from the scanned ID into MeridianLink banking software.

Jack Henry ID verification software

Jack Henry has integrated ID verification and data automation tools into their OpenAnywhere platform, allowing you to streamline account creation.

ID scanning using a Digital Check scanner

Digital Check and IDScan.net have partnered to allow for scanning IDs and parsing data into banking software using your existing SmartSource check scanner.

Authenticate IDs into Argo

Argo has integrated IDScan.net’s document authentication tools, compatible with Thales and Digital Check hardware.

Looking to integrate ID verification or document authentication into your banking or fintech platform?

Banks & Credit Unions

Identity proofing

With our ID scanner for banks and financial institutions, simply scan an ID to quickly, easily, and securely verify customer identity when onboarding new accounts or assessing credit worthiness.

- 2D barcode security checks

- Hologram checks

- Watermark checks

- State format checks

- Data format checks

- Address validation

- DMV data verification

- SSA identity checks

Enhanced due diligence with third party checks

An ID scanner for banks can do more than just scan an ID. It can be paired with deep identity proofing to give you confidence about every individual with whom you do business.

DMV Database Checks

Check customer identity against DMV databases in all available states to confirm ID issuance.

IdentiFraud Checks

Check identity against the SSA, known fraud lists, utility records, and public service records.

Criminal Background Checks

Query court records across the US to perform a criminal background check against a scanned ID.

OFAC Checks

Check against the Office of Foreign Asset Controls list of criminals and money launderers.

PEP List Checks

Determine whether a customer is considered a Politically Exposed Person by checking against the PEP List.

Looking to integrate custom lists or other data sources?

ID verifications for FIs

Leverage ID scanning for in-branch identity verification

Eliminate fat fingers

Parse 100% accurate data from the scanned ID into your teller software.

Reduce identity fraud

Deter fraudsters by confirming identity before withdrawal or loan application.

KYC

Kick off KYC processes by ingesting data directly from the identity document.

AML

Check each customer against OFAC, PEP, and UN sanctions lists.

Catch fake IDs

Use ID authentication to detect up to 95% of fraudulent documents.

Improve processes

Integrate ID scanning into your paperwork processes for improved customer experience.

Benefits of ID scanning for banks

Using an ID scanner at your bank or credit union can greatly improve customer experience.

Detect suspicious IDs

Detect fake IDs by detecting barcode anomalies, or through ultraviolet and infrared ID authentication to catch the vast majority of fakes.

Eliminate typos

No more fat fingers or misspellings. Clean, accurate data is parsed from the ID directly into your CRM or banking software with no need to type.

Reduce paperwork

Save employee manhours and paper by removing the need to make photocopies. Automatically upload an image of the ID directly into the customer profile.

Easy KYC/AML

Perform instant checks against OFAC and PEP lists to do your due diligence to prevent money laundering, avoid fines, and stay compliant with federal standards.

Digital identity verification

Barcode and document security checks

Many tools can read and parse the data on the ID, but our remote ID validation takes it a step further by performing more than 100 algorithmic checks on the ID’s barcode and authentication algorithms to detect potential tampering.

- Data format check

- State “tell” check

- Barcode position check

- Advanced micro-shadow checks

- Jurisdictional check

- Barcode size check

- Front/back crossmatch

- Metadata inspection

Digital identity verification

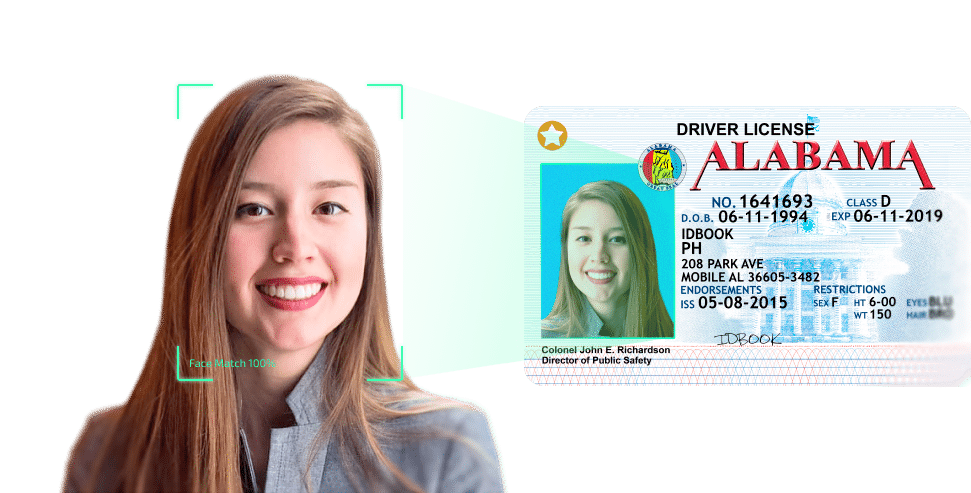

Face matching via selfie

We harness the power of your customer’s mobile phone camera to perform identity verification using a live selfie video. Our face match technology easily confirms that the live user is the same individual as the person in the ID photo.

How long does your face matching take?

The face matching process takes <10 seconds from the time the user opens their mobile camera. The digital identity verification API efficiently creates a mesh template from the ID photo, and then rapidly applies it to the live user on camera, returning a result as soon as it determines whether the face is a match or not.

Does DIVE API face match include anti-spoofing?

Yes. The system performs multiple anti-spoofing checks, protecting against photo attacks, replay attacks, and 3D mask attacks. Click here to learn more about our anti spoofing process.

Does DIVE API face match include liveness checks?

Yes. We offer multiple, randomized liveness checks embedded into the selfie workflow to ensure the individual is a live, legitimate person.

What sets our remote ID validation apart

We pride ourselves on catching the most fake IDs to prevent fintech fraud.

2D barcode security

We check each ID against our template library and AI-algorithms to detect up to 50% of fake IDs from a barcode scan alone.

No per-scan cost

Because we own our own document library, there is no per-scan cost for remote ID validation of North American documents.

Superior OCR

Our OCR is capable of reading and ingesting all text from a document, and instantly compare it to the information in the barcode/MRZ.

Speedy results

Our remote ID validation is lightning fast, which means a smooth, efficient experience for your end customers – no added friction.

Learn how a rapidly growing regional bank implemented digital identity verification during onboarding to greatly reduce fraud.

3 Hill Credit Union implemented VeriScan ID Authentication to address fraud concerns and prevent the use of fake IDs in branch.

LendingUSA, a leading provider of point-of-sale financing solutions, serves thousands of merchants and consumers nationwide.

Paragon Bank moved from manual inspection of IDs to rapid, AI-powered ID authentication with ParseLink.

Need help choosing an ID scanner or remote onboarding tool for your bank?

Our team has worked with banks, credit unions, and other financial institutions and lenders across the country to implement fraud reduction through ID scanning and identity verification.