Skip to content

Skip to content

Scanning ID

Reading New Jersey driver’s license

Identity verified

Document passed all security checks

Data extracted

Parsed fields from document

Sending to banking systems

Transmitting verified identity data

“name”: “Heidi Sample”,

“dob”: “1967-01-12”,

“state”: “NJ”,

“doc_type”: “DL”,

“verified”: true

}

Identity verification for banks and financial institutions

Reduce fraud and identity theft, streamline account opening, and improve customer service with our ID scanners for banks and credit unions.

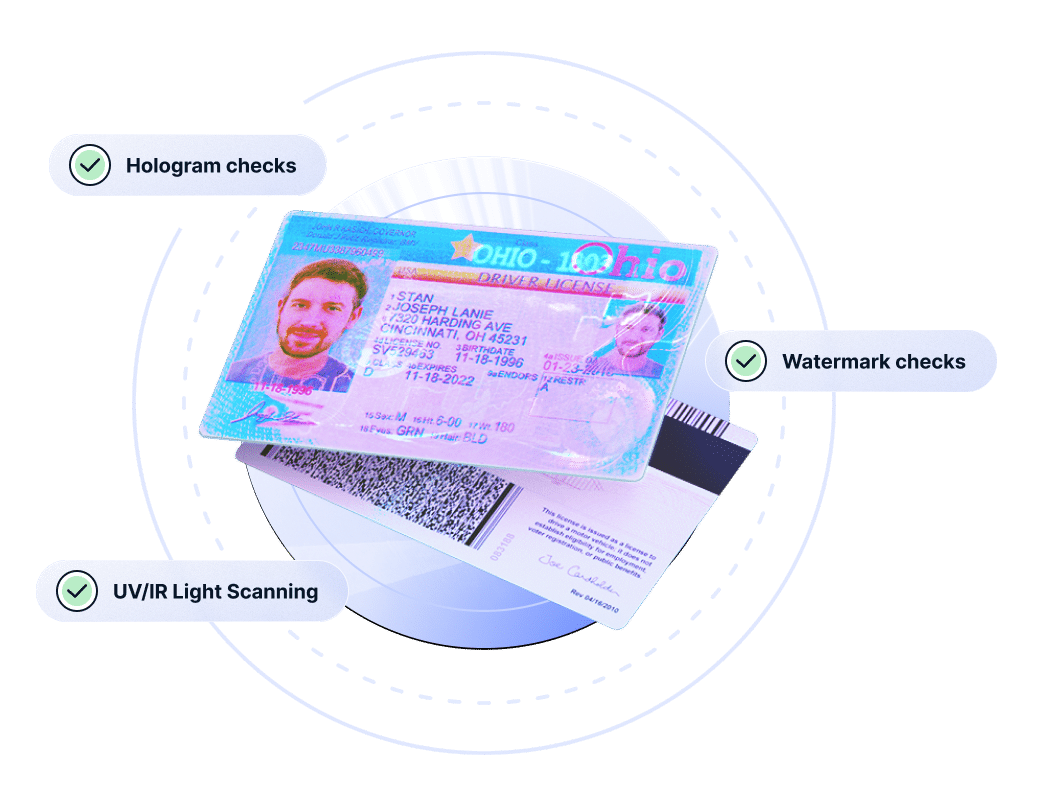

Forensic document analysis to catch the highest percentage of fraud

ID authentication is the deepest level of document analysis available. It examines all present security features on the ID or passport, including security features hidden in the barcode, and security features only present under ultraviolet or infrared light.

- Data syntax check

- Ultraviolet, infrared light analysis

- Barcode position check

- Advanced micro-shadow checks

- Jurisdictional check

- Barcode size check

- Front/back crossmatch

- Metadata inspection

Windowpane Passed

Windowpane Passed  Microprint 600dpi Passed

Microprint 600dpi Passed

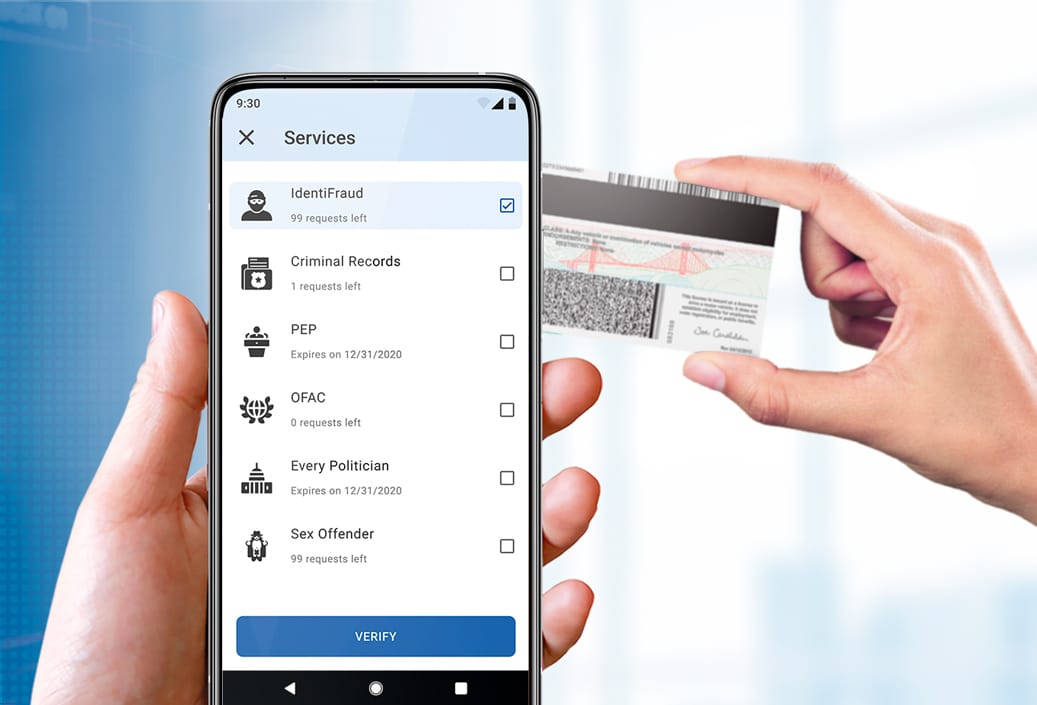

Enhanced due diligence with third party checks

Layer checks against authoritative data sources into your identity verification workflow to ensure compliance with KYC/AML regulations and enhance your understanding of each customer.

DMV database checks

Check customer identity against DMV databases in all available states to confirm ID issuance.

Social Security checks

Check individuals against the SSA database, including death records.

OFAC checks

Check against the Office of Foreign Asset Controls list of criminals and money launderers.

PEP List checks

Determine whether a customer is considered a Politically Exposed Person.

IdentiFraud checks

Perform a wraparound KYC check in a single data query, which can trigger KBA questions.

Telco/utility record checks

Verify whether information on file matches telco and utility billing records.

USPS address checks

Confirm whether the address listed is associated with the individual.

Connect ID scanning to your core banking platform and teller lane software

Add ID scanning software to your bank or credit union tech stack. Prevent ID fraud by verifying every identity document. Clean, accurate data is parsed from the ID directly into your key systems directly from the ID scanner.

- Instantly ingest data

- Save an image of each ID

- Sync data directly into your bank’s key software and systems

- Perform security checks on each ID

- Install in minutes

- Streamline account withdrawals, loans, and other processes

Scan IDs into MeridianLink

Prevent ID fraud by verifying every ID, and then send clean data from the scanned ID into MeridianLink banking software.

Jack Henry ID verification software

Jack Henry has integrated ID verification and data automation tools into their OpenAnywhere platform, allowing you to streamline account creation.

ID scanning using a Digital Check scanner

Digital Check and IDScan.net have partnered to allow for scanning IDs and parsing data into banking software using your existing SmartSource check scanner.

Authenticate IDs into Argo

Argo has integrated IDScan.net’s document authentication tools, compatible with Thales and Digital Check hardware.

Looking to integrate ID verification or document authentication into your banking or fintech platform?

Benefits of ID scanning for banks

Using an ID scanner at your bank or credit union can greatly improve customer experience.

Detect suspicious IDs

Detect fake IDs by detecting barcode anomalies, or through ultraviolet and infrared ID authentication to catch the vast majority of fakes.

Eliminate typos

No more fat fingers or misspellings. Clean, accurate data is parsed from the ID directly into your CRM or banking software with no need to type.

Reduce paperwork

Save employee manhours and paper by removing the need to make photocopies. Automatically upload an image of the ID directly into the customer profile.

Easy KYC/AML

Perform instant checks against OFAC and PEP lists to do your due diligence to prevent money laundering, avoid fines, and stay compliant with federal standards.

Major regional bank leverages DIVE for fraud prevention in account onboarding

“We now have near zero fraud,” says Chief Digital Officer, Alex Carriles.

- Use of DIVE embedded within Jack Henry Open Anywhere software

- Added KYC and DMV checks for best-in-class fraud pevention

- Frontend enhancements for crisp image capture

Regional bank improves teller lane security with ID authentication

After a case of high value fraud, Paragon Bank implemented ID authentication at the teller lane.

- Robust ID verification using the E-Seek M500

- Results are parsed instantly into core banking software

- Easy to read UI helps tellers make quick decisions

Credit union strengthens onboarding with ID verification

Sophisticated fraudsters were testing 3Hill Credit Union’s defenses. ID verification has helped strengthen teller lane security.

- VeriScan at every teller lane and check cashing desk

- Every ID scanned with instant results

- Stops the use of fake or stolen IDs

LendingUSA implements DIVE for loan applications at the point og sale

Point-of-sale financing helps retailers improve conversion rate, but was a fraudster favorite for use of fake IDs. Learn how LendingUSA implemented DIVE to help secure their loan onboarding.

- Prevention of more than 1,000 fraudulent loan applications in the first 12 months

- 90% of applicants processed in 15 seconds or less

Proptech provider MRI launches CheckpointID to stop rental fraud

Every eviction costs multifamily apartment property management companies more than $10,000. MRI leverages ID scanning to prevent fraud before move-in.

- Scanning more than 500,00 ID monthly on iPads

- KYC checks to create a blended risk score

- Millions in bad debt prevented

Scan → Verify speed

~9 seconds

vs. 2-4 minute manual checks

ID types supported

9,700

Drivers licenses, IDs, passports, etc.

Cost of one incidence of fraud

$10,000

FBI estimate

ID verification

Omnichannel identity verification for banks and credit unions

Verify ID and identity remotely

With digital identity verification, you can easily onboard customers, verify identity, and meet KYC/AML standards in seconds. Our three step process includes document validation, and a face matching liveness check.

Scan IDs using the Digital Check SmartSource scanner

The Digital Check scanners are now fully compatible with our ID scanning solutions, allowing for banks to scan IDs into their existing teller lane software with scanners they already have on the floor.

Catch 95% of fake IDs with ID authentication

Specialty hardware can perform forensic document examination under multiple light wavelengths to give deep confidence in the document’s legitimacy.

Query external data sources for deeper fraud protection

We offer easy access to state DMV records, Office of Foreign Asset Control lists, Politically Exposed Persons lists, and a propritary multi-risk check called IdentiFraud which checks identity against more than 15 sources.

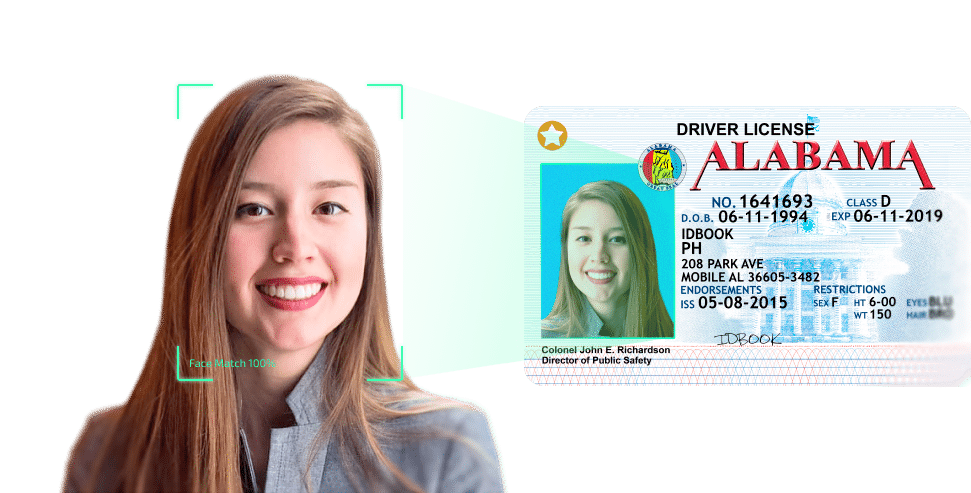

Digital identity verification

Face matching via selfie

We harness the power of your customer’s mobile phone camera to perform identity verification using a live selfie video. Our face match technology easily confirms that the live user is the same individual as the person in the ID photo.

How long does your face matching take?

The face matching process takes <10 seconds from the time the user opens their mobile camera. The digital identity verification API efficiently creates a mesh template from the ID photo, and then rapidly applies it to the live user on camera, returning a result as soon as it determines whether the face is a match or not.

Does DIVE API face match include anti-spoofing?

Yes. The system performs multiple anti-spoofing checks, protecting against photo attacks, replay attacks, and 3D mask attacks. Click here to learn more about our anti spoofing process.

Does DIVE API face match include liveness checks?

Yes. We offer multiple, randomized liveness checks embedded into the selfie workflow to ensure the individual is a live, legitimate person.

Omnichannel ID fraud prevention for banks & credit unions

Our team has worked with banks, credit unions, and other financial institutions and lenders across the country to implement fraud reduction through ID scanning and identity verification.

Integrate your ID scanning with best-in-class hardware and software

We offer ready-made integrations with a variety of software platforms, allowing you to scan IDs, sync data, and prevent fraud within the software your business already uses.